February '24 Market Report

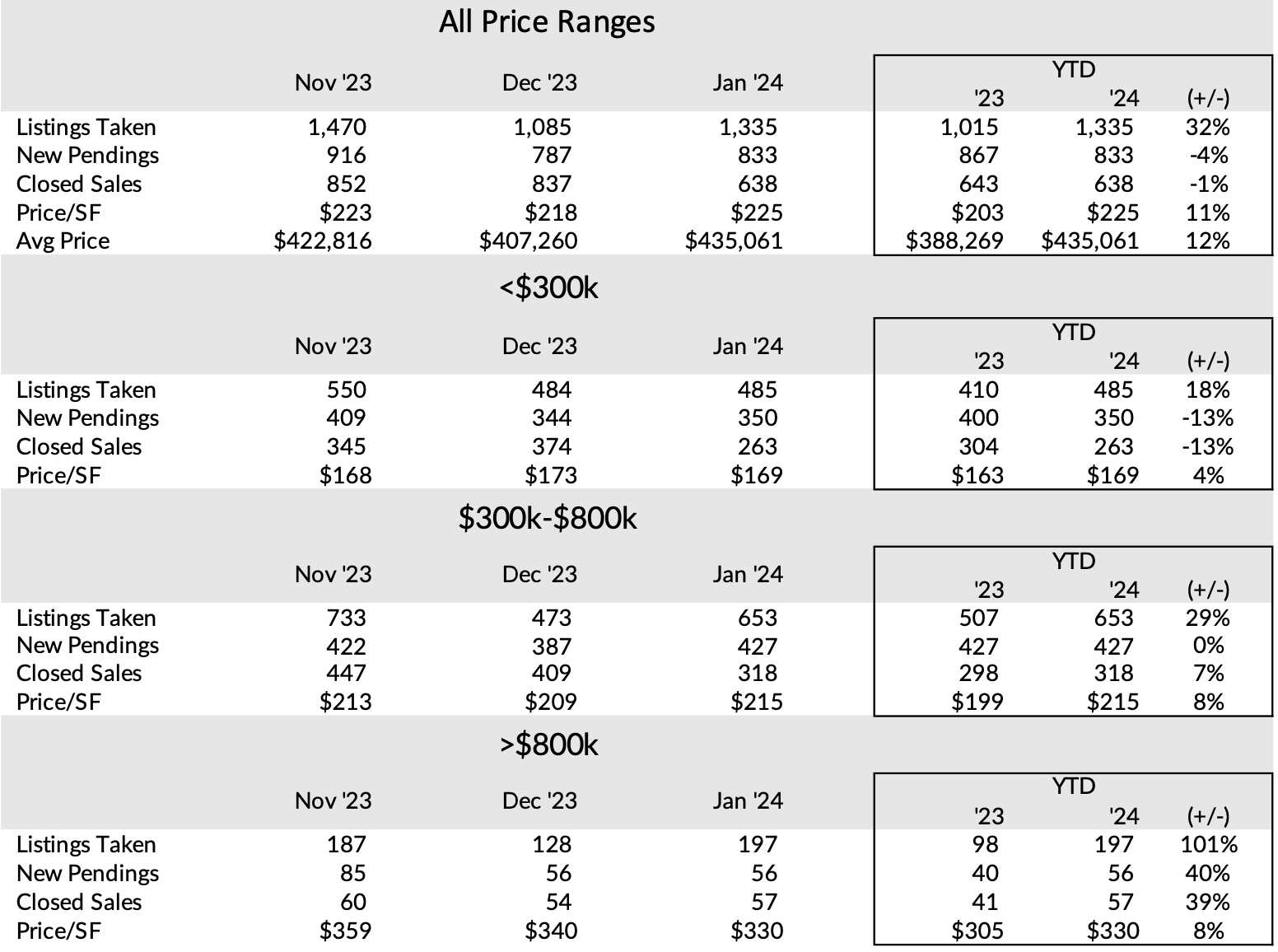

In most markets, the inventory shortages are subsiding some as new listings are more readily available. While January new pendings were up from December, they still lagged behind January of ’23 and January closed sales were slow in most markets.

Looking ahead, with continued strong demand, the additional inventory should boost February pending sales. Expect 2024 to outperform last year in terms of sales. Prices should continue to rise at a moderate pace through the first half.

Most Michigan homeowners recently received their Notice of Assessment for their property taxes. With a 5.1% increase in the 2024 CPI, for the second year in a row, most homeowners will see a 5% increase in the taxable values of their assessments and annual taxes. This is only the second time since 1994 that the CPI capped out at 5%—2023 was the first time.

Michigan Property Taxes in a Nutshell

After several years of rapidly rising prices and mild inflation (until the past two years) homebuyers and sellers need to be aware of the potential for a significant jump between existing taxes and future taxes after the sale.

Michigan’s Headlee Amendment was passed in 1994. Its goal was to limit

tax increases during periods of rapid rising prices so that people with fixed incomes wouldn’t be taxed out of their homes. Headlee limits/caps how much a homeowner’s taxable assessment can be raised—the lesser of the prior year’s rate of inflation or 5%.

State Equalized Values are based on property value. Between 2012 and 2023 property values in Southeast Michigan rose 145%, but capped values (base on inflation) for property owners that remained in their homes during that period rose just 19%.

A seller’s current taxes are usually irrelevant as a predictor of future taxes. Since Headlee, Michigan property tax assessments contain three values:

• State Equalized Value (SEV): 50% of the assessor’s estimate of the true cash value of the home as of December 31st of the prior year.

• Capped Value: Last year’s Taxable Value multiplied by the lesser of the inflation rate or 5%.

• Taxable Value: The lesser of the SEV or Capped Value.

At some point in the past, an assessor estimated the value of each property. Since then, assessors have mathematically adjusted the value based on their sales statistics for that neighborhood. This may go on for years or decades without an assessor revisiting the property.

When a Home Sells: In Michigan, on January first, after a home sells, the previous owner’s Capped Value and Taxable Value are discarded and the SEV (adjusted for last year’s statistical gains or losses for that neighborhood) becomes the new starting point.

What a previous seller or their neighbors paid for taxes is irrelevant. What the buyer pays may also be irrelevant unless: 1.) the SEV is greater than 50% of the sale price; and 2.) the new owner can establish that what they paid is the market/true cash value of the property.